The Great MSME Stimulus Muddle

On May 12, in his televised address to the nation, Prime Minister Narendra Modi announced the Atma Nirbhar Bharat Abhiyan or the “campaign to make India self-reliant,” comprising what was claimed to be a Rs 20 lakh crore package to revive the Indian economy reeling from the effects of an economic recession exacerbated by the all-India lockdown due to the COVID-19 pandemic.

The following day, on May 13, at a media conference, Union Finance Minister Nirmala Sitharaman announced a Rs 3 lakh crore Emergency Credit Line Guarantee Scheme for Micro, Small and Medium Enterprises (MSMEs). Almost a month after the scheme was announced, it is apparent that it lacks clarity, suffering from multiple blind spots and contradictions.

Bankers are in a quandary. Even as the government is wanting banks to lend more to MSMEs and the promoters have queued up to avail of “emergency” credit facilities, banks are finding it practically difficult to implement the scheme. This article seeks to explain why this is happening.

The new loan policy is required to be approved by the boards of directors of banks. However, the full details of the scheme have not been made available yet. On June 1, the Department of Financial Services in the Union Ministry of Finance put out a tweet that Member Lending Institutions (MLIs)––that is, banks and other financial institutions––should reach out to the department on its Twitter account to swiftly resolve their problems and seek clarifications and answers to all their queries relating to the scheme.

The scheme that was announced on May 13, and eventually notified on May 26, had a window for emergency credit distribution between May 23, 2020 and October 31, 2020 or till the full amount of Rs 3 lakh crore is sanctioned, whichever is earlier. It is learnt that the government is having a relook at the five-month window. There is an expectation from the Finance Ministry that the Rs 3 lakh crore disbursal target must be achieved by the end of June. There is pressure on bankers to ensure that this target is met.

Contradictions, Inherent and Internal

The Reserve Bank of India (RBI) is the country’s central bank and apex monetary authority. It is also the regulator of scheduled commercial banks and non-banking financial companies (NBFCs). The RBI sets out systems and procedures for credit delivery. To the best knowledge of this writer, this is the first time that a credit scheme has been designed and rolled out by the Finance Ministry’s Department of Financial Services (DFS).

Under the scheme, the National Credit Guarantee Trust Company Limited (NCGTC), a relatively minor public sector company incorporated in March 2014, is the primary agency through which the scheme is to be operationalised. It may be due to a lack of familiarity with India’s credit delivery systems that the scheme, as it has been laid out, suffers from inherent contradictions.

Consider the following: Under this scheme, MSMEs that each have total loans of up to Rs 25 crore can avail an additional 20% of the loans that are outstanding. This additional loan is termed a “working capital term loan” in the scheme. This structure apparently contradicts the RBI’s existing credit disbursing structure under which working capital loans are currently given to companies.

It was as far back as October 2001, when the RBI had last talked about a “working capital demand loan” (WCDL) system. Subsequently, a “cash credit” method of delivery of working capital by banks to entities has been in force. Under this method, the withdrawal amount is monitored and cannot exceed the “assessed limit,” that is also known as the Maximum Permissible Bank Finance (MPBF) limit. This limit is based on an appraisal of the borrower’s audited balance sheets for previous years, the estimated balance sheet for the current year and the projected balance sheet for the following year. The borrower cannot withdraw the entire amount specified in the MPBF limit without bringing in 25% of the amount as a “margin” from his own resources

However, the Working Capital Term Loan (WCTL) system that the NCGTC is now running is incompatible with the existing system of disbursing working capital through the cash credit method. For instance, if a company is to open a separate WCTL under the scheme, along with the existing cash credit method, then it is unclear which kinds of transactions will be permissible through these loan accounts and which would not. Tracing the end point of the loaned funds is crucial in order to ensure that the funds are not siphoned off or diverted illegally.

Adding fuel to the fire is the controversy that while on the one hand, the NCGTC has said that credit under the new scheme will rank pari passu with existing credit facilities in terms of cash flows (including repayments) and securities, with a charge on the assets financed under the scheme to be created within a period of three months from the date of disbursal, in another breath, it has also said “no additional collateral shall be asked for by MLIs (member lending institutions) for additional credit extended” under the scheme. This confusion is further compounded by the fact that any changes to the current structure of the scheme or its operational guidelines can only be approved by a management committee set up for the purpose by the DFS in the Finance Ministry.

Clearly, a scheme that contradicts itself and existing norms, is bound to leave banks that are supposed to implement the scheme in a quandary. As a result, the stimulus relief this scheme was supposed to bring to the MSME sector has not been realised so far.

Blind Spots and Practical Problems

The scheme also appears to suffer from a significant blind spot in the way it has been framed. According to the scheme, 20% of “outstanding” borrowings can be extended as an emergency credit guarantee. This fails to take into account the question of the status of those borrowings, whether they are classified as stressed or as non-performing assets (NPAs).

For banks, the terms NPA (Non Performing Asset) and SMA (Special Mention Account) are important. SMA-0 and SMA-1 classify the “health” of a borrower account. Specifically, an NPA is a loan or an advance where payments of interest and/or instalments of the principal amount have remained overdue for 90 days or longer in the case of a term loan, and the account is classified as “out of order” in case overdrafts and cash credits are sought.

SMA-0is a category in which both the principal amount and interest repayments have remained outstanding for at least 30 days beyond the due payment date, and is understood to be a level of risk, indicating there may be an incipient stress on the loan account. SMA-1 accounts are those where payments are overdue between 30 days and 60 days, and are considered to be more highly stressed than loans that come under the SMA-0 category.

Sound logic would suggest that lower amounts of emergency credit should be guaranteed to high-risk borrowers while more should be made available to lower-risk borrowers. The government’s new scheme does exactly the opposite, by examining the level of outstanding balance rather than the still available “drawing power/assessed limit” of a borrowers’ account. The following example will illustrate the point being made.

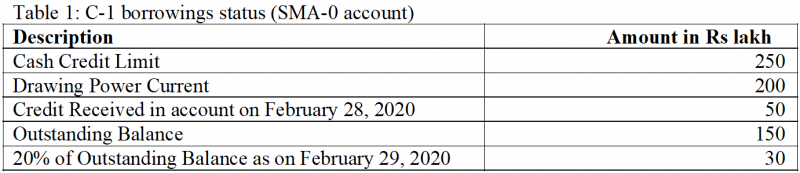

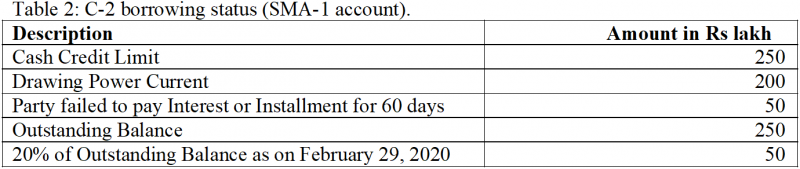

Consider the cases of two hypothetical borrowers, C-1 and C-2. The first, C-1, is an SMA-0 account with its borrowing levels as stated in Table 1. The second, C-2, is an SMA-1 account with borrowing levels as stated in Table 2.

Theoretically, of the two borrowers, C-1, which has an assessed limit of Rs 250 lakh and has a drawing power of Rs 200 lakh, has a better track record being classified as an SMA-0 borrower. However, since it received Rs 50 lakh on February 28, 2020, its outstanding balance would be Rs 150 lakh. Under the new scheme, C-1 will be entitled to a guaranteed credit line worth Rs 30 lakh as a WCLT from the NCGTC (20% of the outstanding amount of Rs150 lakh).

If the government wanted to genuinely help cash-starved MSMEs, it would have been more appropriate to allow banks to lend them 20% of Rs 250 lakh, or at least a similar proportion of the Rs 200 lakh cash credit limit. Here, as a result, a relatively good borrower (C-1) is being “punished.” In the case of C-2, an SMA-1 account that is more stressed than C-1, its own failure to pay inflates the “outstanding” balance resulting in a higher amount (Rs 50 lakh in our example) being made available as an emergency credit line. Thus, the relatively worse borrower is being “rewarded.”

Burden of Loss of Income on Banks

As per Section 6 of the Banking Regulation Act 1949, the term “banking” is defined as monetary transactions for the purpose of lending, taking of deposits of money from the public. For banks, the most important measure of its profitability is “net interest margin” or NIM together with other measures such as “return on assets” and “return on equity.”

Under the Rs 3 lakh crore Rs 3 lakh crore Emergency Credit Line Guarantee Scheme for MSMEs, banks would be contributing 80% of the total amount, the interest rate under the GECL (Guaranteed Emergency Credit Line) is capped at a maximum of 9.25% per annum. What is not, however, clear is whether the interest rate is simple or compound.

To accommodate the low interest rate for loans under the GECL, banks have reduced deposit rates sharply, adversely impacting the interests of depositors, especially senior citizens. Apart from this low rate of interest, there is a moratorium on payment of monthly interest till August 31, 2020.

A petitioner has moved the Supreme Court of India for waiver of interest on the loan amount during the moratorium period on the ground of “right to life” guaranteed by Article 21 of the Constitution of India. Giving an illustrative example in the apex court, the RBI has said on affidavit that banks may have to forego about Rs 2 lakh crore in the form of interest income if it is waived for the six months moratorium period.

This is what the RBI stated in its affidavit: “The weighted average lending rate for banks as on December 31, 2019 was 10.40%, and the outstanding of term loans was Rs 59 lakh crore. Assuming that moratorium is granted to only 65% of the above outstanding (amount), the monthly interest that will be foregone by the banks in case moratorium period has to be declared interest free will be around Rs 33,500 crore…

“Since the moratorium period has been permitted for six months, the total interest income thus foregone will be about Rs 2 lakh crore. This amount is close to one per cent of the national GDP (gross domestic product). And this is only for the banking system, without counting the NBFCs and other financial institutions,” the RBI said, adding that if the banks are required to forego the above amount, there would be huge consequences for the stability of the banking system.

The RBI added that its mandate included protection of depositors’ interests, maintenance of financial stability and ensuring that banks are financially sound and profitable.

Cat Among Pigeons

The so-called stimulus package of loan guarantee schemes for MSMEs has set a cat among the pigeons in the community of bankers. Since procedurally separate loan accounts will be opened for each borrower to whom additional credit is extended under the emergency credit scheme, it is likely to lead to a rush by banks to achieve their required quotas of referrals to particular companies, instead of directing the credit to those companies that most need it.

One strange practical problem that the scheme seems to have overlooked is that it has made SMA-0 and SMA-1 accounts eligible to receive emergency credit, but SMA-2 (payments overdue for 60-90 days) or NPA accounts are ineligible. The cut-off date for the status specified in the scheme is February 29, 2020. This implies that those borrower accounts classified as SMA-0 and SMA-1 on February 29 are eligible to receive emergency credit lines.

It can be argued that that since the scheme was announced on May 13, and notified on May 26, March 31 should have been the corresponding cut-off date for eligibility. As things stand at present, an SMA-0 account, as on February 29, may have become an SMA-2, and an SMA-1 account as on February 29, and may have become an NPA by March 31, 2021. Banks are not supposed to extend fresh credit to accounts classified as NPA. It is not surprising then that they are in a big dilemma because following the new loan scheme’s terms may demand that bankers flout extant norms.

According to a report in the Hindustan Times on June 10, public sector banks had till then sanctioned loans worth only Rs 1,109 crore to MSMEs in 12 states under the Emergency Credit Line Guarantee Scheme. Of this amount, Rs 599 crore has already been disbursed to 17,904 accounts, according to data compiled by the DFS. The report added that sanctions and disbursements were low because of inadequate demand.

Rewinding of Reforms Big Cause of Concern

This contradictory and confusing emergency credit scheme is being imposed on public sector banks at a time when they are already under stress. With uncertainty looming large, banks have approached the Union Ministry of Corporate Affairs (MCA) seeking fast-tracking of 40 resolved, high-value insolvency cases in which decisions from the bankruptcy courts under the Insolvency and Bankruptcy Code are pending.

The woes of India’ banking sector have been mounting in recent years: from increasing provisions for rising NPAs to scandals relating to the working of several banks, including Yes Bank and the Punjab and Maharashtra Cooperative (PMC) Bank. Whereas these problems can be attributed to underlying structural issues in the Indian economy, the kind of targeted lending to MSMEs envisaged by the emergency credit line scheme is likely to worsen the financial health of public sector banks, straining an already strained banking system. The NPA burden on the MSME sector, which currently stands at 12.5%, is certain to go up in the near future.

In a meeting with bankers on May 23, Finance Minister Sitharaman urged banks to extend loans automatically to eligible borrowers without fear of the “3Cs” that is the CBI (Central Bureau of Investigation), the CVC (Central Vigilance Commission) and the CAG (Comptroller and Auditor General of India).

What this means for banking regulation in the future remains to be seen. Will the Ministry of Finance usurp the powers of RBI? Will bankers really be unafraid of the three Cs? Who will be the disciplinary and punitive authorities when things go wrong? Time will perhaps provide answers to these questions.

The author is a CAIIB (Certified Associate of the Indian Institute of Banking and Finance), has 37 years of work experience in the private sector and in a nationalised bank, and is the All India Deputy General Secretary of the All India Bank Officers’ Confederation.

Get the latest reports & analysis with people's perspective on Protests, movements & deep analytical videos, discussions of the current affairs in your Telegram app. Subscribe to NewsClick's Telegram channel & get Real-Time updates on stories, as they get published on our website.