Soaring Steel Prices, Credit Crunch Bleed MSMEs

A pre-engineered building constructed by Halleys Blue Steel Pvt. Ltd

From buildings and bridges to tunnels and consumer products, like automobiles and others, steel has a pivotal role in the manufacturing sector, including the Micro, Small and Medium Enterprises (MSMEs).

MSMEs purchase steel either from retailers or wholesalers depending on the size of the order. If the requirement is large enough, around 400-500 metric tonne (MT) per month, they can place orders directly with the manufacturer—the Steel Authority of India (SAIL), Tata Steel and JSW Steel Ltd, the largest steel producers in the country.

The pandemic has severely impacted MSMEs, which are reeling under the demand shock and the doubling of steel prices. “Pre-COVID-19, the price of steel was around Rs 37,000-Rs 40,000 per metric tonne. Now, it costs Rs 90,000. Domestic steel manufacturers seem to have formed a cartel,”

S Sampathraman (80), former president, Federation of Karnataka Chambers of Commerce and Industry (FKCCI), tells Newsclick.

Sampathraman is also the CMD of Bengaluru-based DPK Engineers Pvt Ltd, which manufactures diesel generators and generally caters for realtors. The spike in steel prices is a big blow to his business because cold rolled steel sheets are used to produce the various components of a diesel genset.

Another former FKCCI president K Shiva Shanmugam (65), who is also the CEO of Shiva Shakti Engineering Company, purchases steel directly from manufacturers. “How is it possible that all the steel manufacturers are quoting the exact same price? There should be some difference if it’s an open market,” he says.

Shanmugam runs two factories in Karnataka that manufacture mild steel barrels, which are used primarily to store oil and petroleum products. He buys around 300 MT of mild steel (MS) sheets, the primary input for his products, per month directly from JSW and SAIL. “In February 2021, the price of MS sheets was around Rs 45,000 per MT. By July-August, it doubled to R 90,000. Steel manufacturers are hurting the domestic market by mostly exporting their products,” he adds.

In 2019, China was the world’s largest exporter of steel. However, Beijing opted to cut down production and steel exports to reduce carbon emission in 2021, which has benefited Indian manufacturers.

According to Shiva Murthy (64), the MD of Bellary-based Halleys Blue Steel Pvt Ltd, the situation turned “horrible” in the last two years. Yet he has refused to lay off his 150 employees, who manufacture made-to-order, prefabricated industrial buildings for customers who want a factory or warehouse in a short duration. Almost 90% of the construction material in such buildings is steel. “Our pre-pandemic turnover of around Rs 40-Rs 50 crore per year has sharply dropped by more than 30%.”

Murthy, who purchases around 400-500 MT of steel per month directly from JSW, says, “The prices of hot rolled plates, GP coils and colour coated roofing sheets have doubled,” adding that the guaranteed emergency credit line (GECL) loan he took was insufficient to meet his expenditure. “Demand has dried up and orders have reduced.”

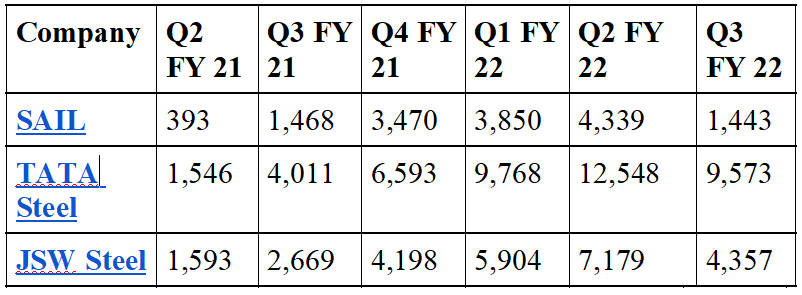

Meanwhile, steel companies have reported record profit in the last four quarters. The table below shows the net profit (in crore) of the largest steel companies in India. The data has been extracted from financial reports.

Emergency Credit Facilities

After the first lockdown, DPK Engineers laid off almost two-thirds of its 350-strong labour force. After posting losses for two consecutive years, the company is also facing a cash crunch with customers paying late, making it harder to meet operational expenses.

To inject working capital and help restart businesses,

the Narendra Modi government had launched the Rs 3 lakh crore Emergency Credit Line Guarantee Scheme (ECLGS) in May 2020. Under the scheme, banks and NBFCs can provide collateral-free GECL loans to MSMEs with the government providing the guarantee. MSMEs can borrow up to 20% of their entire outstanding credit (as on February 29, 2020) up to Rs 25 crore.

However, according to businessmen, banks allegedly release miniscule amounts of credit and ask for additional guarantees in the form of collateral given earlier by the firms—in contravention of the scheme guidelines. Moreover, banks reject applications on the basis of CIBIL scores from previous year’s performance, they further allege.

DPK Engineers, Halleys Blue Steel and Shiva Shakti Engineering had all obtained GECL loans during the pandemic to meet the working capital requirements of their businesses. Though the loans helped them stay afloat, the companies say that the line of credit was insufficient to meet their needs.

“How is it that the big players can take thousands of crores of loans without offering any guarantee? But in the case of MSMEs, the banks ask for balance sheets, CIBIL scores and audit reports only to reject the application,” says Shanmugam.

KE Raghunathan, convenor, Consortium of Indian Associations, says the scheme has been faulty from the outset. “First, lockdown (and restrictions) lasted for six months. Merely giving 20% of the outstanding loan as credit was not enough. Second, borrowers who come under SMA-2 were not eligible for GECL. Only regular, SMA-0 and SMA-1 were eligible. Therefore, ailing MSMEs did not get loans,” he says.

SMA in banking is a special mention account that is exhibiting signs of stress, resulting in the borrower defaulting on his debt obligations. SMA-1 is an account that has defaulted on interest or principle for 31-60 days. SMA-2 is an account that has defaulted wholly or partially for 61-90 days. When the default period crosses 90 days, the account is classified as an non-performing asset (NPA).

“These loans have increased my liability—I used them to pay salaries, rent and so on. But how can I repay the loans unless I generate profit? Will an entrepreneur be able to revive his business when there is uncertainty in the market?” a frustrated

Raghunathan asks.

“The government should have relaxed the conditions for entrepreneurs further instead of only a one-year moratorium on repayment. After the second wave, the government increased the credit facility by 10% but this was not enough. The second wave lasted almost four months. Therefore, accounts that were regular or SMA-1 in 2020 had become NPA by 2021,” Raghunathan says.

Banks are risk averse

Zico Dasgupta, assistant professor of economics, Azim Premji University, says banks are rationing credit to MSMEs due to the NPAs amassed by large corporations. “The credit-to-deposit ratio has been consistently falling since 2019,” Dasgupta, a macroeconomist looking at macro trends in the economy, including the banking sector, tells Newsclick. The credit-to-deposit ratio shows how much a bank is lending for every unit of deposit. A higher ratio implies that the bank is lending more either due to a higher demand or higher capacity.

According to Dasgupta, a ratio of around 75%-78% may be considered low risk. In March 2019, (for the entire banking sector, excluding NBFCs), the ratio was 78%. In March 2020, it fell slightly to 75% and in the same month in 2021, it was 72.5%. As on November 5, 2021, it dropped to 69.6%. This shows how the banking sector has become risk averse due to the pandemic as well as the NPA burden. Coincidentally, the last time the ratio was this low was during the week after demonetisation in 2016.

MSMEs have a significant role in the economy. According to government estimates, the share of MSMEs in GDP was 30.5% in 2018-2019 and 30% in 2019-2020. Replying to a question raised by Congress leader and MP Rahul Gandhi in Parliament in 2021, the government had said that 9% of MSMEs had shut down during the pandemic. However, Raghunathan claims that an All India Manufacturers’ Association internal survey (with 46,525 respondents) in 2020 found that 35% of MSMEs could not survive. A Consortium of Indian Associations survey (with 87,000 respondents) in 2021 found that 30% of units were shutting down.

Under the Atmanirbhar Bharat Package in May 2020, definition of MSMEs was changed with firms with a turnover of up to Rs 250 crore categorised as medium-sized units, Rs 50 crore small and Rs 5 crore micro. The 2006 definition classified units based on the size of investment, not turnover. As per government estimates, there are 6.3 crore MSME units.

According to the Economic Survey 2021-2022, Rs 2.28 lakh crore had been disbursed to 95.2 lakh borrowers till November 19, 2021. In the latest Budget, the size of ECLGS was expanded to Rs 5 lakh crore and the scheme was extended till March 2023.

Dasgupta suggests that the government should spend more partly by charging higher corporate tax on large corporations. “In 2021, the total corporate tax concession was 3.9% of GDP, which is huge—around Rs 5 lakh crore. This is greater than the corporate tax collection, which is around 3% of GDP,” he says.

Credit facilities were not always linked to balance sheets, Dasgupta adds. “Till the 90s, we used to have development financial institutions whose credit disbursal policies would not depend on a profit motive. After 1998, all banks (including in the public sector) linked their credit disbursal to profit making. The idea of development financial institutions was to subsidise credit. The finance and banking market is biased against those with low assets. The government is unable to mitigate the threats to MSMEs.”

Get the latest reports & analysis with people's perspective on Protests, movements & deep analytical videos, discussions of the current affairs in your Telegram app. Subscribe to NewsClick's Telegram channel & get Real-Time updates on stories, as they get published on our website.